LJUNG-BOX AUTOREGRESSIVE MODEL FOR THE RETURNS OF THREE NIGERIAN INSURANCE COMPANIES’ STOCKS

Mots-clés :

Insurance , Model , Price , Return , StockRésumé

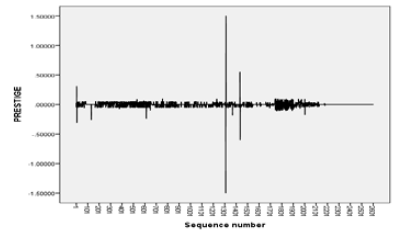

ANCHOR, MANSARD and STACO insurance companies’ return pattern in Nigeria were analyzed using the statistical package for social science (SPSS). The data for this study was got from the daily closing prices of the stocks of these companies between 2006 and 2018. The daily returns were computed and the analysis done using Time Series. Stationarity were detected when the plots of the return series were plotted. The Autocorrelation and Partial Autocorrelation plots were used to identify the models as well as the order of the

models for the three Insurance companies. The Autoregressive model of order two was fitted to the returns on ANCHOR and STACO stocks respectively. While MANSARD had Autoregressive model of order three fitted to it. The adequacy of the model was tested using Ljung-Box test by observing the residual plot. The results proved that the models suited the data.

Publiée

Comment citer

Numéro

Rubrique

Comment citer

Articles les plus lus par le ou les mêmes auteur/ices

- A. O. Abam, O. Izuchukwu, TIMETABLE REMINDER: AN OFFLINE ANDROID ALGORITHM , FULafia Journal of Science and Technology : Vol. 3 No 1 (2017): Fulafia Journal of Science and Technology (FJST)

- A. O. Abam, E. F. Nsien, C. I. Umeobioha, MARGINAL ANALYSIS OF THE DEMAND OF SEASONAL/ PERISHABLE GOODS: A SINGLE-PERIOD INVENTORY MODEL APPROACH , FULafia Journal of Science and Technology : Vol. 5 No 2 (2019): Fulafia Journal of Science and Technology (FJST)

- O. A. Ayeni, E. F. Nsien, A DISCONNECTED DRINK INVENTORY MANAGEMENT PROGRAMME , FULafia Journal of Science and Technology : Vol. 3 No 1 (2017): Fulafia Journal of Science and Technology (FJST)

Articles similaires

- Adenomon M. O. , Adehi M. U. , Dantani Aminu Asambe, Nweze N. O. , MODELLING TIMES SERIES VOLATILITY: A CASE STUDY OF NIGERIA ECONOMIC VARIABLES , FULafia Journal of Science and Technology : Vol. 9 No 2 (2025): Fulafia Journal of Science and Technology (FJST) (In Progress)

- Y. Dauna, S. I. Mshelia, A. A. Akinrefon, PRICE FLUCTUATION AND SPATIAL MARKET INTEGRATION OF RICE IN ADAMAWA STATE RICE MARKET , FULafia Journal of Science and Technology : Vol. 5 No 2 (2019): Fulafia Journal of Science and Technology (FJST)

- Usman Mohammed Yusuf, Collins E. Akpan, Ibrahim Musa Saleh, M. M. Yalwa, Blessing Toyin Enoch, Mathematical Modeling of the Spread of the Ebola Virus Disease , FULafia Journal of Science and Technology : Vol. 8 No. 2 (September, 2024): Fulafia Journal of Science and Technology (FJST)

- S. O. Sule, A. O. Sotolu, S. A. Okunsebor, S. O. Sanusi, AQUACULTURE INSURANCE IN SUSTAINABLE FISH PRODUCTION: CASE STUDY OF NIGERIA AGRICULTURAL INSURANCE CORPORATION, OYO STATE , FULafia Journal of Science and Technology : Vol. 5 No 2 (2019): Fulafia Journal of Science and Technology (FJST)

- M. U. Olanipekun, A. J. Olanipekun, K. A. Amusa, A. J. Opeodu, PARAMETERS EXTRACTION OF A DOUBLE-DIODE MODEL OF PHOTOVOLTAIC CELL USING NEWTON-RAPHSON METHOD , FULafia Journal of Science and Technology : Vol. 4 No 2 (2018): Fulafia Journal of Science and Technology (FJST)

- Samuel Owoweye, Folasade Durodola, Taofeek Adetoro, Babatunde Bisiriyu, Mahrufdeen Adegbenro, REAL-TIME IDENTIFICATION OF MAIZE PLANT AND WEEDS USING MACHINE LEARNING MODEL IMPLEMENTED VIA YOLO v5 , FULafia Journal of Science and Technology : Vol. 8 No. 2 (September, 2024): Fulafia Journal of Science and Technology (FJST)

- Mbe E. Nja, E. C. Nduka, P. U. ogoke, DESIGNING AN OFFSET POISSON-GAMMA MIXTURE REGRESSION MODEL , FULafia Journal of Science and Technology : Vol. 1 No 1 (2015): Fulafia Journal of Science and Technology (FJST)

- D. H. Aku, A. M. Alhamdu, P. F. Useni, DERIVATION OF FITZHUGH-NAGUMO SYSTEM , FULafia Journal of Science and Technology : Vol. 2 No 2 (2016): Fulafia Journal of Science and Technology (FJST)

- K. I. Falade, ON MATHEMATICAL PROJECTION OF NIGERIA POPULATION USING NUMERICAL TECHNIQUES , FULafia Journal of Science and Technology : Vol. 5 No 2 (2019): Fulafia Journal of Science and Technology (FJST)

- O. A. Olasunkanmi, Hezekiah O. Adeyemi, Olaolu Folorunsho, LINEAR PROGRAMMING APPROACH TO MODELING FOUNDRY CUPOLA FURNACE CHARGE , FULafia Journal of Science and Technology : Vol. 6 No 2 (2020): Fulafia Journal of Science and Technology (FJST)

Vous pouvez également Lancer une recherche avancée de similarité pour cet article.